A Look Back at Union Pacific

A Look Back at Union Pacific

A railroad that went nowhere

A little over a year ago I analyzed Union Pacific UNP 0.00%↑ and decided to pass because I did not believe the company was appropriately valued.

A year on and the company’s shares have gone essentially nowhere, and so perhaps its time to look back on the company and see if anything has changed.

You can read the original analysis here:

Let’s get started.

The Thesis

The first thing we need to take into consideration is to see what I thought about the company, and what my thesis for the investment was:

This is a boring stable business unlikely to be disrupted

The company is heavily constrained by labor relationship and regulations

The company is a cash cow, rather than by investing in additional expansion

Debt has been going up, which is a mistake. The debt is floating rate too.

They have been conducting share buybacks at high valuations

The dividend is fine and will continue to be raised

The company is simply too expensive at this time

How has this held up?

Let’s take it point by point:

This is a boring stable business unlikely to be disrupted

Well this hasn’t changed at all.

Railways continue to be the most efficient method of transporting goods over long distances over land, and that’s really unlikely to change anytime soon.

Additionally the costs of expansion continue to be extremely high, which means that UNP 0.00%↑ is not going to see any new competitors show up on its doorstep anytime soon… and it hasn’t.

The company is heavily constrained by labor relationship and regulations

So it is, and this has caused some issues recently, though at least for now the railways have managed to keep the state on their side.

Still, this is and will continue to be an ongoing issue, and concern going forward. Just because they rolled the dice of government intervention and it came up positive this time doesn’t mean it always will.

And of course, they will likely be negative affected by incoming legislation resulting from the Ohio derailment.

For now though, nothing has changed here.

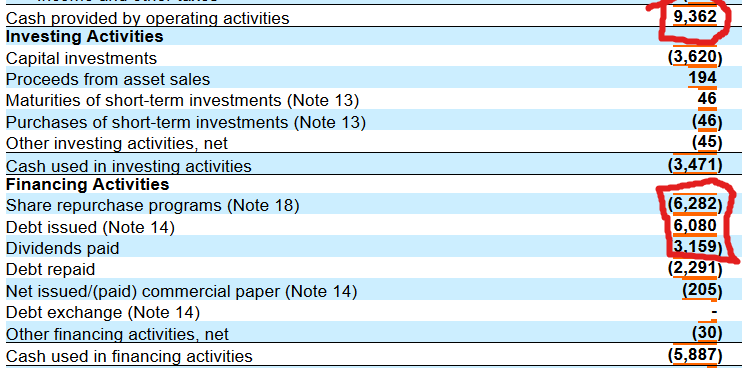

The company is a cash cow, rather than by investing in additional expansion

On the one hand the company spent more cash on Capital Expenditures in 2022 than they did the prior year, on the other hand they increased dividends and have continued to put out enormous share buybacks…

Indeed if we add it up we can see that they spent more cash on buybacks and dividends than they made in operating cashflow, meaning they had a significant amount on negative free cash flow… Which brings us to the next point:

Debt has been going up, which is a mistake. The debt is floating rate too.

They keep adding to their debt pile.

In particular they are adding to their debt pile while conducting share buybacks:

This is stupid, and a terrible allocation of capital.

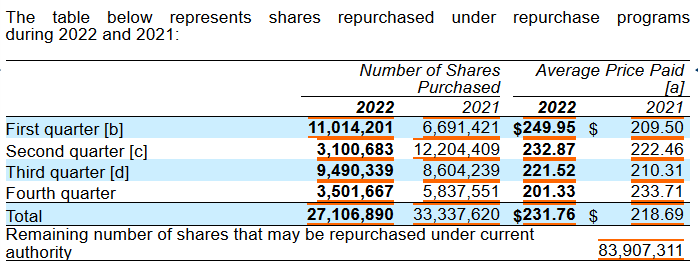

They have been conducting share buybacks at high valuations

Why?

Because they’re taking on debt at a 4.95% interest rate to buy back stock that’s got a lower yield! This is literally destroying capital.

Look, I like share buybacks, they’re a great tool, but only if the company is undervalued.

Additionally taking on debt to make these buybacks is a risky decision, and really not good when you’re making the buybacks at such high prices.

It’s really quite simple here:

Earnings Yield - 4.8%

Dividend Yield - 2.2%

Interest rate - 4.95%

Even in the best case scenario you’re trading in a 4.95% expense for a 4.8% gain, meaning you’re losing out on 0.15%!

And that’s not even considering the fact that the 4.95% you’re paying in interest is risk-free, whereas the 4.8% you’re getting is certainly not risk free.

Is it possible that earnings will jump tremendously next year and that will salvage this? Maybe, but i doubt it.

This is a bad allocation of capital.

The dividend is fine and will continue to be raised

Fortunately dividends don’t really have this issue!

There’s enough free cashflow to pay out these dividends (assuming they quit buying back overpriced stock), and certainly enough earnings too.

I think they will continue their dividend policy for the foreseeable future.

The company is simply too expensive at this time

This hasn’t really changed despite the slight decrease in share price since my initial analysis.

I like railroads, but at least right now UNP 0.00%↑ is a bit too pricy for my tastes, particularly given the massive mis-allocation of capital that has been ongoing with these buybacks.

Maybe I will take another look if it goes down to $100 per share or so.

The future

Overall the company has turned out about what I expected.

It’s a fine company that’s only really hamstrung by its high stock price, and poor capital allocation decisions.

I’d like it if they were to take a step back from these buybacks and started paying down this debt, while continuing their dividend raises.

That said, it’s a solid company, and I think that any investors looking to receive steady and rising dividends will likely continue to be happy shareholders.

Current Stance: HOLD

What do you think UNP 0.00%↑ should do?